The ACORD form has undergone recent changes, and with these changes come questions about how to interpret the new form. bcs offers some basic tips and instructions for one of the most commonly misinterpreted and misleading parts of the new ACORD form - the additional insured and waiver of subrogation columns.

The Additional Insured and Waiver of Subrogation Columns

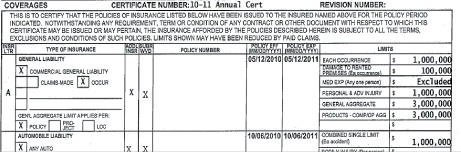

In the sample certificate below, the insurance agent has placed an “X” inside of the additional Insured and waiver of subrogation columns. This “X” could either indicate that there is coverage, or there is not coverage. What if the agent had marked “√”, or even “+”? Are these symbols ambiguous? Agents may have their own idea as to when their symbol of choice means there is coverage, and when it means there is not coverage; however, the burden ultimately falls on the risk manager to evaluate the meanings of these different symbols, on hundreds or even thousands of certificates. For this reason, ACORD has issued guidelines for insurance agents to follow when issuing a certificate of insurance.

ACORD Guidelines

ACORD guidelines state that in the additional insured column on the certificate, agents should enter “Y” for yes, if there is coverage and “N” for no, if there is not coverage. This is the standard for indicating whether or not a policy includes additional insured or waiver of subrogation coverage. The “Y” and “N” can be clearly understood by all who read the certificate. Agents should not be using ambiguous marks such as “X,” “√,” or “+.”

Remember, regardless of what’s indicated in the columns of the certificate, the certificate itself is not proof of the coverage. You need copies of the actual vendor’s general liability policy additional insured and waiver of subrogation endorsements in order to confirm whether or not the policy extends that coverage. An ACORD certificate only provides you with an indication of what the insurer and agent intended to convey.

As we discussed in prior articles, the Acord 25 (2009/09) states:

“If the certificate holder is an ADDITIONAL INSURED, the policy(ies) must be endorsed. If SUBROGATION IS WAIVED, subject to the terms and conditions of the policy, certain policies may require an endorsement. A statement on this certificate does not confer rights to the certificate holder in lieu of such endorsement(s).”

What this means for you is two-fold. First, examining only a certificate is not proof of coverage. If you are unsure as to whether the proper additional insured, waiver of subrogation, or other policy endorsements are in effect, the only way to know for sure is to collect and inspect those physical endorsements. Second, keep in mind that on the certificate of insurance, agents should not use ambiguous marks and symbols to indicate coverage, as outlined by ACORD.